Medicare, the federal insurance plan for older Americans, provides healthcare coverage for Americans 65 and older. Medicare also covers certain younger people with disabilities and those with End-Stage Renal Disease (sometimes called ESRD). Although it’s the most widely-used health insurance plan in the United States, Medicare never fails to confuse many pre-retirees who are approaching their 65th birthday.

Medicare Part A (along with Part B) makes up “Original Medicare”, which is provided by the federal government. Most doctors take Part B, and nearly all eligible older Americans are enrolled in Original Medicare.

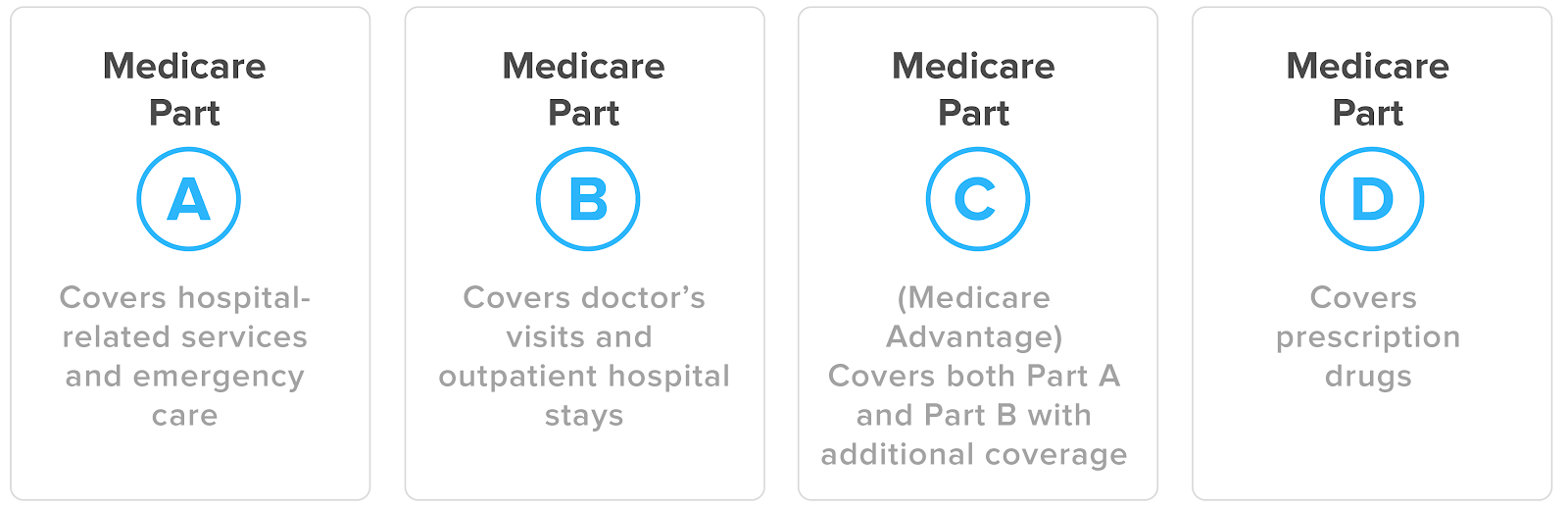

The Four “Parts” Of Medicare

Medicare is divided into four different parts, designated with letters A, B, C, and D.

- Medicare Part A is hospital insurance. It covers hospital stays and services provided by skilled nursing facilities along with home health care and hospice.

- Medicare Part B is outpatient medical insurance. Part B coverage applies whenever you see your doctor, receive outpatient care, or obtain preventive care.

- Medicare Part C, known as “Medicare Advantage,” provides coverage to older Americans through private insurance companies, contracted by the federal government.

- Medicare Part D provides prescription drug coverage.

Important Terms to Know

Original Medicare: Referring to Medicare Part A and Part B altogether.

Benefit Period: The time period during which a patient is hospitalized for an extended stay. Also referred to as “spell of illness” a benefit period starts on the day you are admitted to the hospital. It ends when 60 days have passed since discharge from either hospital care or care from a skilled nursing facility. There is no limit to the number of benefit periods you can have. There is also no limit to how long a benefit period can last.

Medicare will cover up to 100 days of skilled nursing facility care in a benefit period.

Part A Deductible: Instead of operating in yearly cycles, the Part A deductible for hospitalization applies to each benefit period.

Who Is Eligible for Medicare Part A Coverage?

If You’re 65 Years and Older:

The main group for which Medicare was set up. To qualify for Medicare (and premium-free Part A), you need to fulfill two requirements:

- You must have been a U.S. citizen or permanent resident for more than five years, AND

- You must have paid Medicare taxes for at least 10 years.

If You’re Younger than 65 Years Old:

There are a few cases where people under the age of 65 are eligible to get Medicare benefits. To qualify, you’ll need to belong to one of three groups:

- You’re permanently disabled, and you’ve received Social Security Disability Insurance (SSDI) for at least the last two years; OR

- You’re suffering from end-stage renal disease (ESRD)/end-stage kidney disease and need to undergo continuous dialysis or need a kidney transplant; OR

- You receive Social Security disability benefits for amyotrophic lateral sclerosis (ALS)/Lou Gehrig’s disease.

What Does Medicare Part A Cover?

Inpatient Hospital Care

Medicare Part A coverage includes inpatient hospital care at any of the following types of facilities:

- General hospitals;

- Long-term care hospitals;

- Acute care or critical access hospitals;

- Rehabilitation facilities (inpatient); and

- Psychiatric hospitals.

Hospital coverage includes Semi-private rooms; meals; general nursing care, medications administered during your hospital stay, and additional hospital services or supplies that are medically necessary for your care.

Skilled Nursing or Rehabilitation Facilities

Part A coverage for a temporary stay in a skilled nursing facility (SNF) is subject to strict criteria:

- Your stay at the SNF must come within 30 days of a hospital stay AND that hospital admission should have lasted at least three days. (For example, if you were admitted into a hospital on July 1, you must stay at least until July 4. If you’re required to go to a skilled nursing facility after discharge, Medicare will cover your nursing home costs only if you check-in to an SNF between July 4 and August 3).

- If there is a skilled need, the first 20 days are fully covered, but days 21 to 100 require that you pay up to $200 a day in coinsurance (based on rates for 2023.).

- You’re covered for up to the first 100 days of your stay at a skilled nursing facility, but ONLY if you require a “skilled need” or skilled nursing or skilled therapy – on average, Medicare covers about 20 days. For example, if you need injections or physical therapy for a period of time, Medicare will contribute to your costs at a SNF but only as long as you need skilled nursing or therapy, up to 100 days.

Hospice Care

Part A covers hospice services for terminally-ill patients, which can be provided in a variety of settings, including the home, an assisted living facility, or an inpatient hospice facility. You are eligible for Part A hospice coverage if:

- You have a terminal illness (with a life expectancy of six months or less) or

- You agree to accept hospice care in lieu of other Medicare-covered treatments.

There is a 5% co-insurance payment required for respite care costs and covered medications. Otherwise, Part A covers all the costs.

Home Health Services

Medicare Part A covers short-term health services provided in your home, including:

- Physical therapy,

- Occupational therapy,

- Speech therapy, and

- Intermittent skilled nursing care.

The patient must be considered homebound and meet other criteria.

What Is Not Covered by Medicare Part A?

Part A covers many procedures and services during hospitalization, but it doesn’t cover:

- Most dental care;

- Eye examinations related to prescribing glasses;

- Dentures;

- Cosmetic surgery;

- Acupuncture; and

- Hearing aids and related exams.

How Much Does Medicare Part A Cost?

Premium (Cost Per Month)

Monthly premiums for Part A are $0 for people who have worked long enough to qualify for Social Security benefits (people who paid Medicare taxes for at least 10 years). People who don’t qualify for Social Security (those people who didn’t pay Medicare taxes) pay a monthly premium for their Part A coverage.

Deductible

For each hospital stay, Medicare Part A beneficiaries need to fulfill a Part A deductible (a fixed amount paid out-of-pocket) before Medicare begins to cover the cost of that hospital bill. For benefits associated with skilled nursing facilities, home health services, or hospice care, Medicare beneficiaries do not have to pay a deductible.

How Does Medicare Part A Interact with Other Medicare Programs?

Part A and Part B:

- Part A and Part B are a standard part of every Medicare Plan. Original Medicare – Part A (hospital insurance) and Part B (medical insurance) – are complementary. Parts A and B coverage do not overlap.

- Since Medicare Part B comes with a monthly premium cost, some people choose to delay enrollment in Part B. There is no penalty for delaying enrollment in Medicare Part B if you or your spouse have other coverage through an employer.

- If you enrolled in Part A and delayed signing up for Part B, you can enroll in Part B during a Special Enrollment Period (SEP). Your SEP begins at the earliest date at which you or your spouse stop working or coverage ends. The SEP ends eight months later.

Part A and Medicare Supplement (Medigap):

- Medicare Supplement Insurance (Medigap) policies are overseen by the government but run by private companies.

- Medigap policies can help Medicare enrollees pay out-of-pocket costs which Medicare Part A and Part B don’t cover, such as copayments, coinsurance, and deductibles.

Part A and Medicare Advantage (Part C):

- Medicare Part C is not a separate benefit; rather, it’s an alternative to Original Medicare. Part C enables private health insurance companies to provide Medicare benefits through what are known as Medicare Advantage plans. That is, you can choose to get your Medicare coverage via a Medicare Advantage Plan instead of through Original Medicare.

- Medicare Advantage Plans must offer at least the same benefits as Original Medicare (those covered under Parts A and B), but may stipulate different rules, costs, and coverage restrictions.

Part A and Part D (Prescription Drug Coverage):

- Original Medicare (Part A and Part B), does not cover most medications. You can get prescription medication coverage by enrolling in a stand-alone Medicare Part D Prescription Drug Plan.

How Do I Enroll in Medicare Part A?

If you’re under 65 years old and have received Social Security Disability Insurance (SSDI) for the past 24 months:

- You will be enrolled automatically in Medicare Parts A and B at the beginning of your 25th consecutive month on SSDI.

- If you are immediately eligible due to ALS or ESRD, you will be automatically enrolled in Part A and B once your benefits begin.

- Your Medicare ID card should arrive in the mail around 90 days before your Medicare start date.

If you’re already receiving Social Security or benefits when you become eligible for Medicare (i.e. upon turning 65 years old):

- You will be enrolled automatically in Medicare Parts A and B, and coverage takes effect on the first day of the month you turn 65. An exception to this occurs if your birthday falls on the 1st of the month. In that case, your Medicare coverage will start one month prior to your birthday (i.e. if you turn 65 on May 1st, your Medicare coverage will start April 1st).

- Your Medicare ID card should arrive in the mail about 90 days prior to your Medicare start date.

If you aren’t receiving Social Security when you become eligible for Medicare (i.e. upon turning 65 years old):

- If you’re not currently receiving Social Security benefits, don’t expect to be notified when it’s time for you to sign up. Your enrollment in Medicare isn’t automatic–you will need to apply for Part A and Part B coverage.

- You can apply online on the Social Security website, or over the phone by calling the Social Security Administration at 1 (800) 772-1213.

Enrollment Periods: When Can I Sign Up for Medicare Part A?

Initial Enrollment Period

If you aren’t receiving Social Security and approaching age 65, you can enroll in Part A during your Initial Enrollment Period (IEP).

- The IEP is a seven-month period; the fourth month being the one in which you turn 65.

- You can enroll in Medicare starting up to three months before your 65th birthday and your window to sign up ends three months following your 65th birthday. (eg. If your 65th birthday is April 20, your IEP begins January 1 and ends July 31.)

Special Enrollment Period

If you delayed Medicare enrollment when turning 65 because you were insured through an employer for whom you or your spouse was still actively working — you need to sign up for Medicare during a Special Enrollment Period (SEP).

- The SEP allows you to sign up for Medicare starting at any point before your or your spouse’s employment ends, up until eight months following your (or your spouse’s) retirement.

- If you are younger than 65 and lose your employer-sponsored health coverage when your older spouse retires and signs up for Medicare, you will need to find separate coverage for yourself.

General Enrollment Period

If you do not qualify for premium-free Part A and did not enroll during your Initial Enrollment Period, you can sign up during a General Enrollment Period.

- The General Enrollment Period lasts from January 1 through March 31.

- You’ll sign up using the same process as a first time Medicare enrollee, but you may have to pay higher premiums for delaying coverage.

This period also applies to those who did not enroll in Part B initially at age 65 and do not qualify for a Medicare Special Enrollment Period. In both cases, a late enrollment penalty will apply.